Wealth is an obstacle for parents to navigate. A perennial advantage becomes a burden in the domain of parenting.

In ‘David and Goliath’, Malcolm Gladwell examined the relationship between income and parenting. He argued what we all would expect to be true: it’s hard to parent effectively when you are struggling to pay the bills. Money makes parenting easier, until a certain point. And then it stops making much of a difference.

What is surprising is that that point is $75,000 USD, after which, ‘diminishing marginal returns set in’.[1]

‘If your family earns an extra $25,000 more than your neighbour, you can drive a nicer car and go out to eat more often. But it doesn’t make you happier or better equipped to do the thousands of small and large things that make for being a good parent.’[2]

What is even more interesting is that the difficulty associated with parenting follows an inverted U-Curve, where greater wealth actually brings greater challenges.

Figure 1: The Relationship between Wealth and Ease of Parenting

To support his argument, Gladwell captures the story of a wealthy self-made man in Los Angeles. As a parent, this billionaire reflects that ‘children in wealthier families find it harder to learn the value of money, the meaning of work, and the joy and fulfilment that comes from making your own way in the world.’

All parents want to teach their kids to be well adjusted and appreciate the value of money. We find that people with no money talk about it all the time, either directly or indirectly, because it shapes so many decisions. Even when it’s not verbalised, it doesn’t take long in a decision-making conversation to realise that the internal dialogue is related to cost.

People with a lot of money prefer not to talk about it at all. Many of our clients struggle with the conversation, something we explored in ‘We need to talk about the wealth’.

The concept of the inverted U-Curve is something we often discuss with families and when we do, we typically get the same type of responses. Firstly, people focus on the fact that the figures are U.S.-centric, arguing that it costs more to raise a child in Australia. Secondly, people just don’t believe the correlation to be true. Or more accurately, but unspoken, they don’t believe it is true for their family, but may be true for wealthier families.

We are going to explore both of these objections and test whether the gut reaction we encounter has any grounding, or if the science is simply an inconvenient truth. Let’s dive in.

1. It costs more to raise a child in Australia

First of all, Gladwell uses U.S. dollars, so we need to account for exchange rates. Doing so at the end of 2016 takes his pivotal family income to $100k AUS.

The cost of living in Australia is higher and also needs to be reflected in the numbers. To calculate this difference, we looked at some useful metrics including the consumer price index and The Economist’s ‘Big Mac’ index. Taking the average of three data points, we calculated a cost of living mark up in Australia of 11%.[3] This takes the tipping point in our Australian model to $110k.

When we talk about expenditure, people specifically argue that the cost of raising a child is greater in Australia. It was hard to find comparable data between the U.S. and Australia, but we found two reports that capture a similar range of spend for middle-income families. The U.S. study was based on one child, so we normalised the cost to align to the two-child family in the Australian study we found. Once the calculations were complete, the average costs per year were within $2,000 of each other. All in all, the cost of a child really isn’t any more expensive in Australia.

It is interesting to note that some cultural norms creep into the statistical approach. The Australian data covers costs to age 24, perhaps reflecting the increased number of children who stay at home when completing tertiary education, while U.S. statistics cut off at 18. Here is a breakdown:

|

USA |

Australia |

| Source |

U.S. Department of Labor, 2006 – Updated to 2011 dollars using the Consumer Price Index |

2013 National Centre for Social and Economic Modelling |

| Middle Income |

$107,853 |

$118,248 |

| Family Size |

2 Children

U.S. 1-child figures have been doubled, with a 19% reduction for 2 children to match AUS approach |

2 Children |

| Total Cost |

$579,053 (to 18yrs) |

$812,043 (to 24yrs) |

| Avg. cost per year |

$32,169 |

$33,835 |

Figure 2: U.S. – Australia cost of raising a child. (Note all $AUD at Dec 2016 exchange rates)

Australian costs in more detail

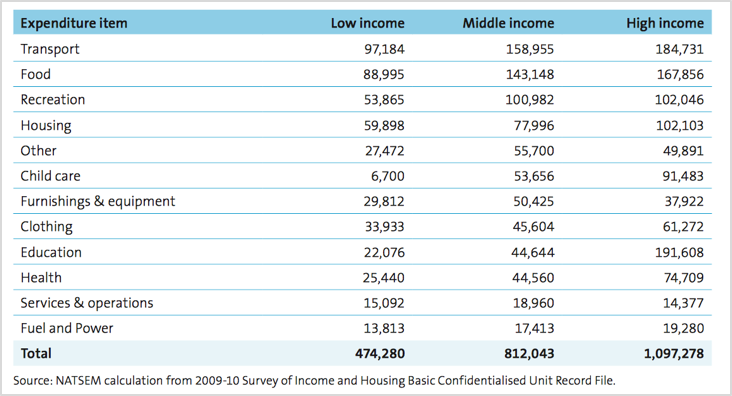

When we shift focus to the cost of raising a child in a high-income family (average family income of $5,000 per week), the spend rises to $1,097,278 or $45k a year for two children. This expenditure covers a comprehensive range of costs.

Figure 3: Lifetime shopping bill for two children from birth until they finish their education.

The main differences between income groups stem from Education, Childcare, Healthcare and Transportation. Education is the biggest gap, with $170k of greater expense for a high-income family than a low-income family (likely even greater for most people).

In summary, with adjustments for the Australian dollar, Australian cost of living and the cost of raising a child, the total presented by Gladwell moves from $75,000 USD to $110,000 AUD. So there is a difference, but it’s marginal.

I can’t genuinely accept that correlation

Malcolm Gladwell is a great writer; he captures the science simply alongside compelling anecdotes, so it’s easy to go along with his arguments without exerting too much critical thinking. One of the main data points that he draws upon is the correlation between happiness and wealth. He points to the research which demonstrates that when you reach a certain level of wealth, your happiness plateaus.

In actual fact, the research here is a little more complex than the parallels Gladwell draws. Daniel Kahneman and Angus Deaton studied 450,000 people against two types of subjective well being – emotional and life evaluation.[4]

- Emotional: the quality of everyday experience – the frequency and intensity of joy, stress, sadness, anger and affection that makes one’s life pleasant or unpleasant.

- Life Evaluation: thoughts people have about their life when they reflect on it.

Life evaluation rises with income. When we pause and reflect, people with greater financial resources feel happier. Emotional wellbeing on the other hand rises with income, but there is no further progress beyond an annual income of $75,000 USD.

Gladwell could argue (he doesn’t do so explicitly) that emotional wellbeing dictates parenting ability, and that day-to-day emotional wellbeing is the critical component. I might add that patience, if it is considered emotional wellbeing, is close to the top of the list.

Let’s assume that the relationship between wealth and emotional wellbeing explains the first half of the U curve and the plateau. This doesn’t account for the challenge as wealth increases. This is the pivotal component. Why does parenting become harder as wealth increases?

The psychologist James Grubman explains the second half of the curve: ‘A parent has to set limits. But that’s one of the most difficult things when you don’t have the excuse of, “we can’t afford it, it’s gone”. “No we won’t” is much harder. “No we can’t” is simple. You have to say, “Yes, I can buy that for you. But I choose not to”. It’s not consistent with our values. But that requires that you have a set of values, know how to articulate them, and know how to make them plausible to your child. All of which are really difficult things for anyone to do.’[5]

This argument resonates with our experiences working with families. As well as helping facilitate the conversations Grubman describes, focusing on values is powerful because it helps a family appreciate how much it has in common.

Still don’t believe it?

It is important to remember Gladwell focuses on just one part of being a parent – instilling the value of money and the meaning of work.

It is no more heartening when we turn to empirical studies by Suniya S. Luthar which demonstrate that the challenge for wealthy children is not just constrained to finding the joy and fulfilment that comes from making their own way in the world. Luthar reports that ‘wealthier children tend to be more distressed than lower-income kids, and are at high risk for anxiety, depression, substance abuse, eating disorders, cheating and stealing. Compared to National rates, boys and girls from families with an income greater than $150k have serious levels of depression, anxiety, or somatic symptoms twice as often or more.’[6]

Conclusion

The correlation we have examined here may be negligible between our Australian tipping point of $110k and a family income of say $250k. After all, the curve arches away slowly as the wealth axis increases. At the same time, greater wealth does bring greater challenges; it is something we witness firsthand.

For families where wealth is a new phenomenon, and for parents who didn’t necessarily strive to be ‘rich’, these challenges can be greater. Families with a history of successfully transferring wealth between generations often have a set of family norms that help to nurture stewardship. Parents who are new to wealth may not naturally have the skills or experience to manage the transition for their children.

Many of us live in a certain bubble that insulates us from the national or global reality of our status, with a confirmation bias that filters out arguments such as these. It is important therefore to reflect on whether we might benefit from a slightly different tack with our children, even if the challenges are not immediately obvious day-to-day, and if the statistics in front of us are a little inconvenient.

[1] Malcolm Gladwell, David and Goliath, 2014

[2] Ibid.

[3] 11% is calculated by combining the average of the following data points:

– Consumer price index including rent (6% higher in Australia)

– Restaurant prices (11.57% higher in Australia)

– Purchasing-power parity from the Economist Big Mac index (14.6% lower in Australia)

[4] Daniel Kahneman, Angus Deaton: ‘High income improves evaluation of life, but not emotional wellbeing’, 2010

[5] Malcolm Gladwell, David and Goliath, 2014

[6] Suniya S. Luthar Ph.D. Psychology Today, June 2016